"„Fljótt flýgur fiskisaga.“ The 1,020-króna Haddock"

There's an Icelandic saying: „Fljótt flýgur fiskisaga.“ — a fishy story travels fast. This week it travelled across two morning-radio interviews and turned one real number into a market. Here's what the auction data actually shows. (All prices ISK/kg; USD in brackets at Central Bank of Iceland rates, ≈126 ISK/USD in mid-2026.)

It started, as these things do, with a phone call to a morning show. A small-boat fishermen's chairman was asked the eternal question: why is fish getting so expensive? His answer was, honestly, pretty good economics. Low supply. Russia squeezed out of EU markets. Norwegian quota cuts year after year, cod cuts domestically. Costs up across the board — fuel, gear, everything it takes to land a fish — but yes, he admitted, the boats are doing well out of it. He made the point every buyer three time zones away forgets: 95%+ of Icelandic fish is exported, so the price is set in competition with foreign markets, not by what an Icelander pays at the counter. Asked specifically about haddock, he was refreshingly honest: he hadn't looked into it, he'd just noticed the price looked high — "on par with cod."

The next day, a fish processor picked up the thread. She'd been in the trade a few years and had never seen prices like this — haddock especially, she said, had rocketed after Easter and hit 1,020 ISK/kg (~$8.1) for whole fish at the auction. From there she built an honest, brick-by-brick cost stack: at 1,020 raw, after handling fees, freight, tub rental, filleting, trimming, packaging, rent and utilities, she'd need to sell around 4,100 (~$33) — and, she reckoned, by the time a fish shop adds its margin the shopper pays roughly 6,000 ISK/kg (~$48).

None of this is a hit piece. Both of them were more careful than most. But a number got loose — 1,020 — and by the second interview it had quietly become "the price of haddock." So we pulled the auction data. Here's how the story holds up.

"Fish is expensive right now" — true

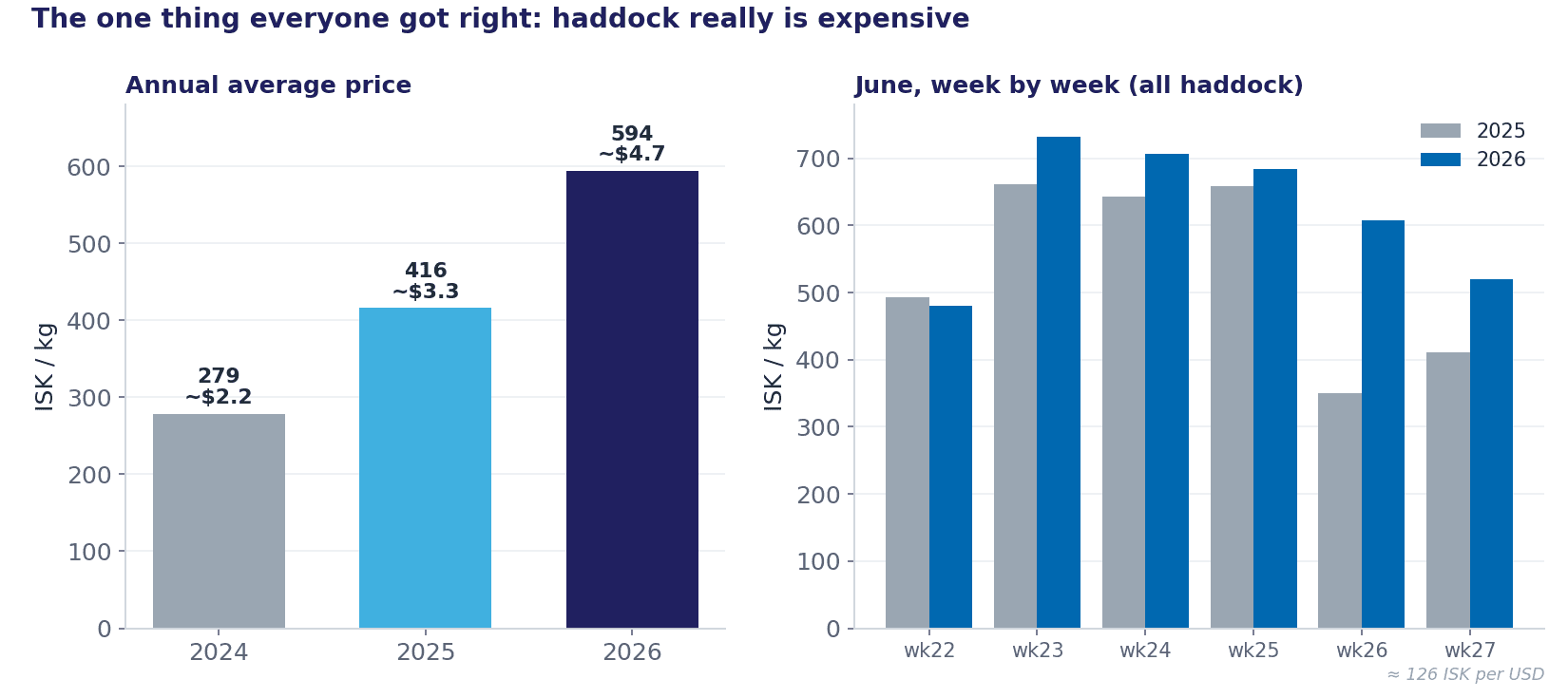

The macro story checks out. Volume-weighted across every size, gear and condition on Icelandic auctions, haddock has gone from 278 ISK/kg (~$2.2) in 2024 to 416 (~$3.3) in 2025 to 594 (~$4.7) so far in 2026 — more than double in two years. June 2026 sits above June 2025 in almost every week, and haddock auction throughput tightened sharply mid-month — down roughly 60% year-on-year in weeks 24–25 before recovering later in June. Less fish through the middle of the month, firmer prices. The chairman's supply-and-demand read is exactly what the data says.

Icelandic haddock, volume-weighted ISK/kg (USD ≈126 ISK/USD). Left: annual average. Right: June week by week. Source: Oceans of Data — RSF auction data.

Holds up

The market is genuinely tight and expensive. On the headline, both of them are right.

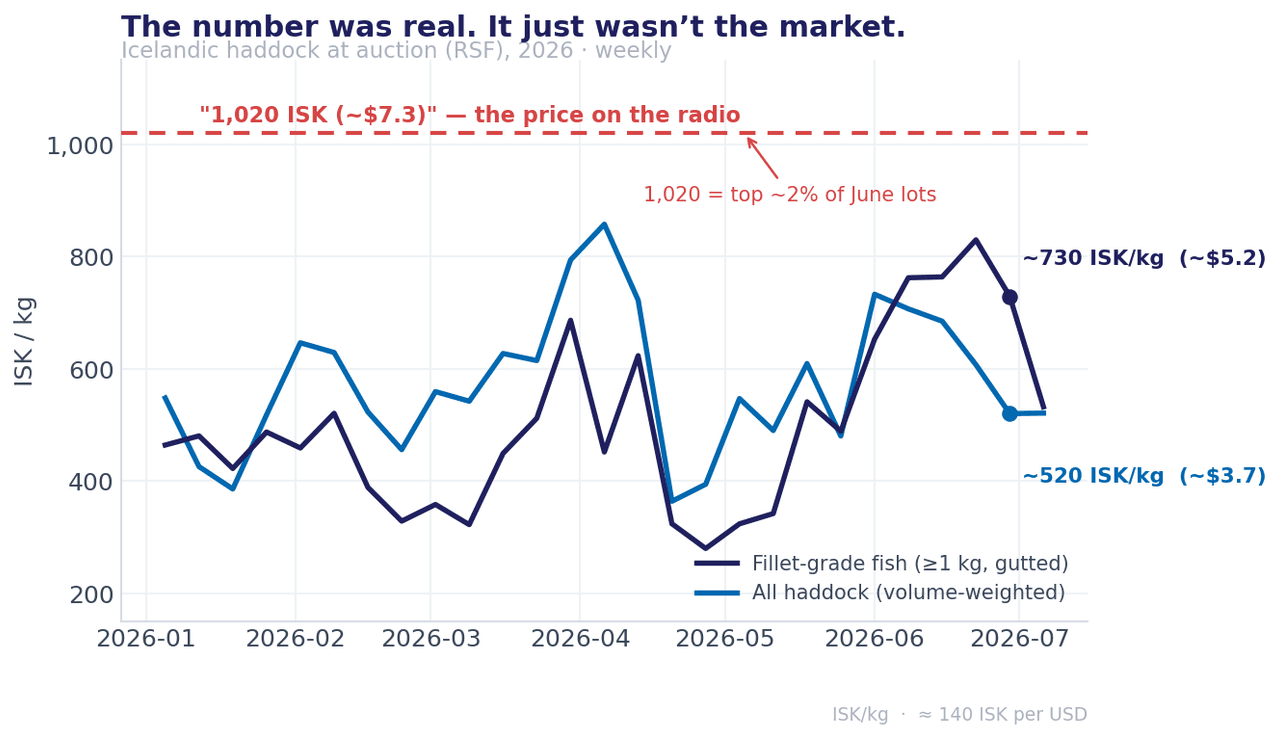

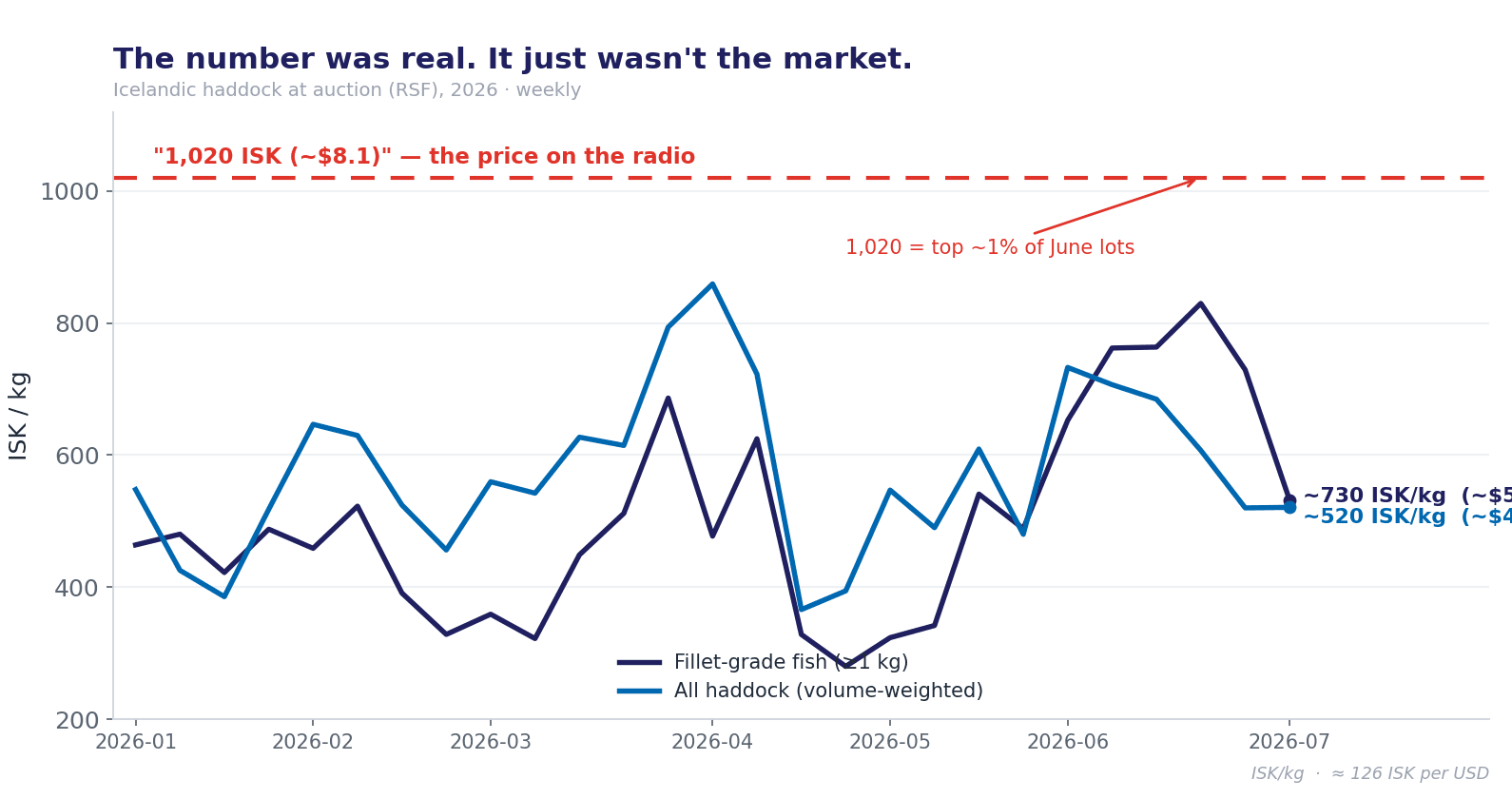

"1,020 for whole haddock" — real, but it's the top, not the market

Here's where the fish story starts to swim. 1,020 (~$8.1) is not invented — top-grade lots really did trade there in June. But it's the top of the range, not the middle of it. Whole haddock across all of Iceland's auctions in the last complete week averaged about 520 ISK/kg (~$4.1). Even the larger, fillet-grade fish (≥1 kg) averaged around 730 (~$5.8), peaking near 830 (~$6.6). Lots at 1,020 or above made up just ~1% of June's volume.

The red line is the number on the radio. Neither the whole market (blue) nor the larger, fillet-grade fish (navy) gets near it. Source: Oceans of Data — RSF auction data.

So the 1,020 she cited is a real top-lot price on a strong week — that part is true. What travels is the sentence with the label filed off: "haddock hit 1,020" makes the market sound twice as hot as the volume-weighted reality. That's the fishy story flying. Not a lie — a real number that grows in the retelling.

Real, mislabelled

1,020 is a top-1% lot price, not "the price of haddock." Against the market it's ~2×; against the larger, fillet-grade fish, ~25–40% high.

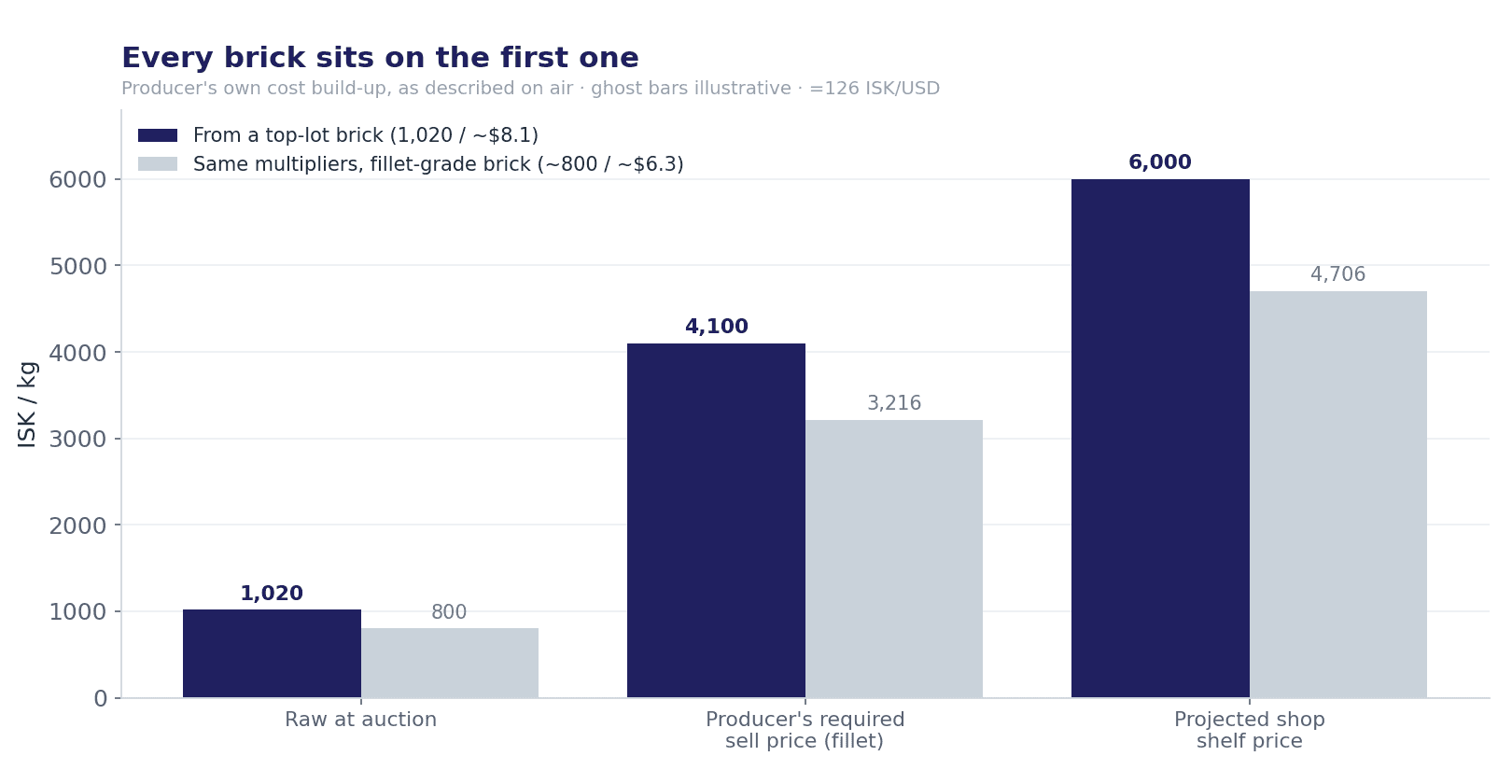

Why the label matters: every brick sits on the first one

The cost stack was the honest part — and exactly why the starting number matters so much. The 4,100 (~$33) and 6,000 (~$48) are her own cost-plus figures — what she'd need to charge, and what she reckons a shop would then charge — not retail prices we've measured. What the data can confirm is the brick they're built on: 1,020 is the top ~1% of the market, not the 520 (~$4.1) all-in average or the 730 (~$5.8) fillet-grade average. And every brick above it is a multiple of that first one. Run the very same multipliers off a fillet-grade brick (~800 / ~$6.3) and the projected shelf price lands closer to 4,700 (~$37) than 6,000. The tower is honest arithmetic; it's just built on a top-lot foundation.

The producer's own build-up, as described on air. Ghost bars apply the same multipliers to a fillet-grade starting price — illustrative only, not measured retail. Source: Oceans of Data — RSF auction data.

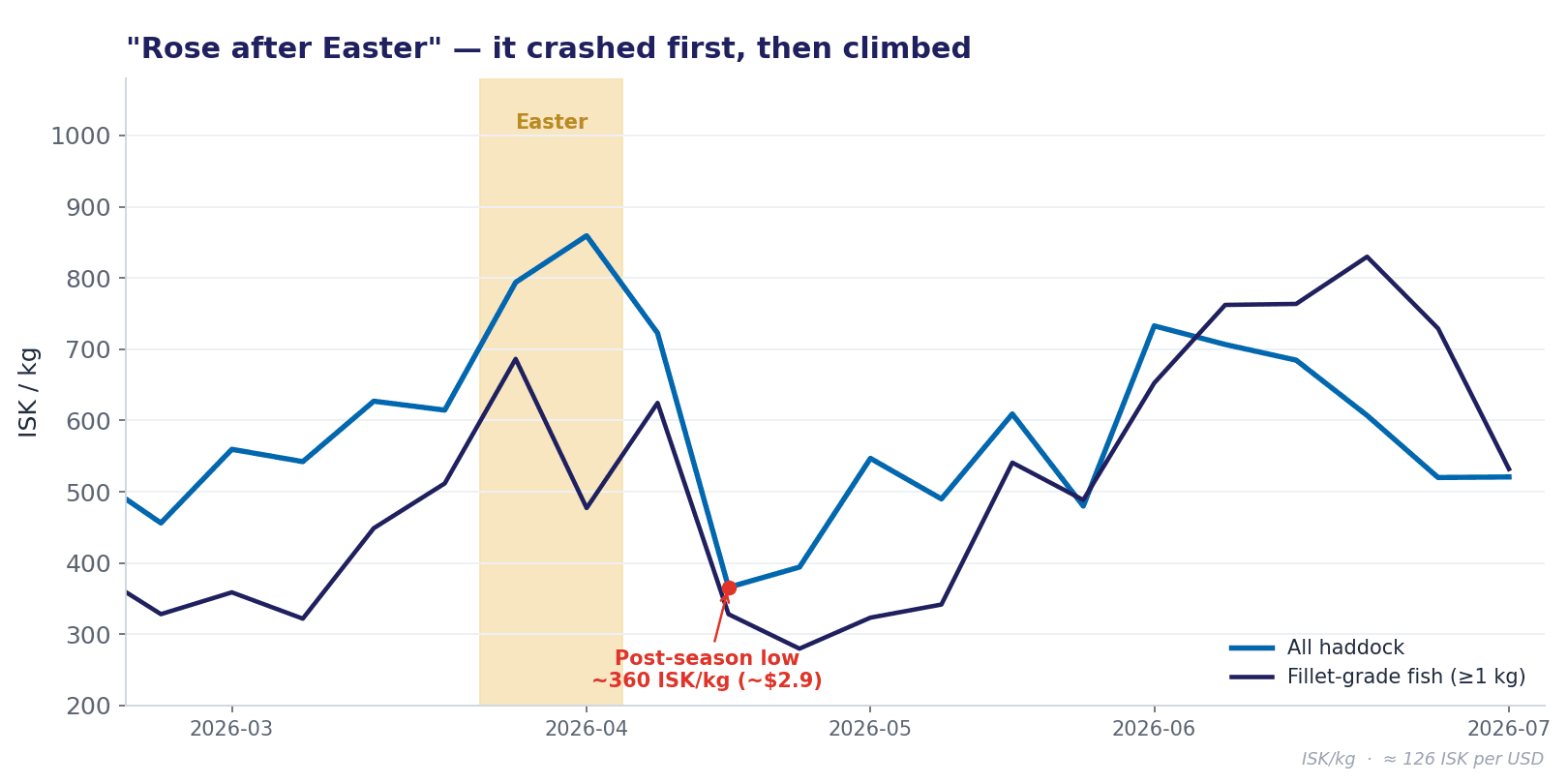

"Rocketed after Easter" — down first, then up

The direction got a little lost at sea. Prices didn't climb straight after Easter — the whole-market average crashed to the year's low near 360 ISK/kg (~$2.9) as post-season landings flooded in. Only then, as supply tightened through May and June, did it climb back. For the larger, fillet-grade fish, the move off that late-April floor really was dramatic — more than double — so "rocketed after Easter" is fair if you measure from the trough. Measured from Easter itself, it dipped before it flew.

The post-Easter move was down, then up. Order of operations matters. Source: Oceans of Data — RSF auction data.

Half true

The larger grades did climb steeply — off the post-season low, not because of Easter. The timing in the story is reversed.

The bit the radio never has time for

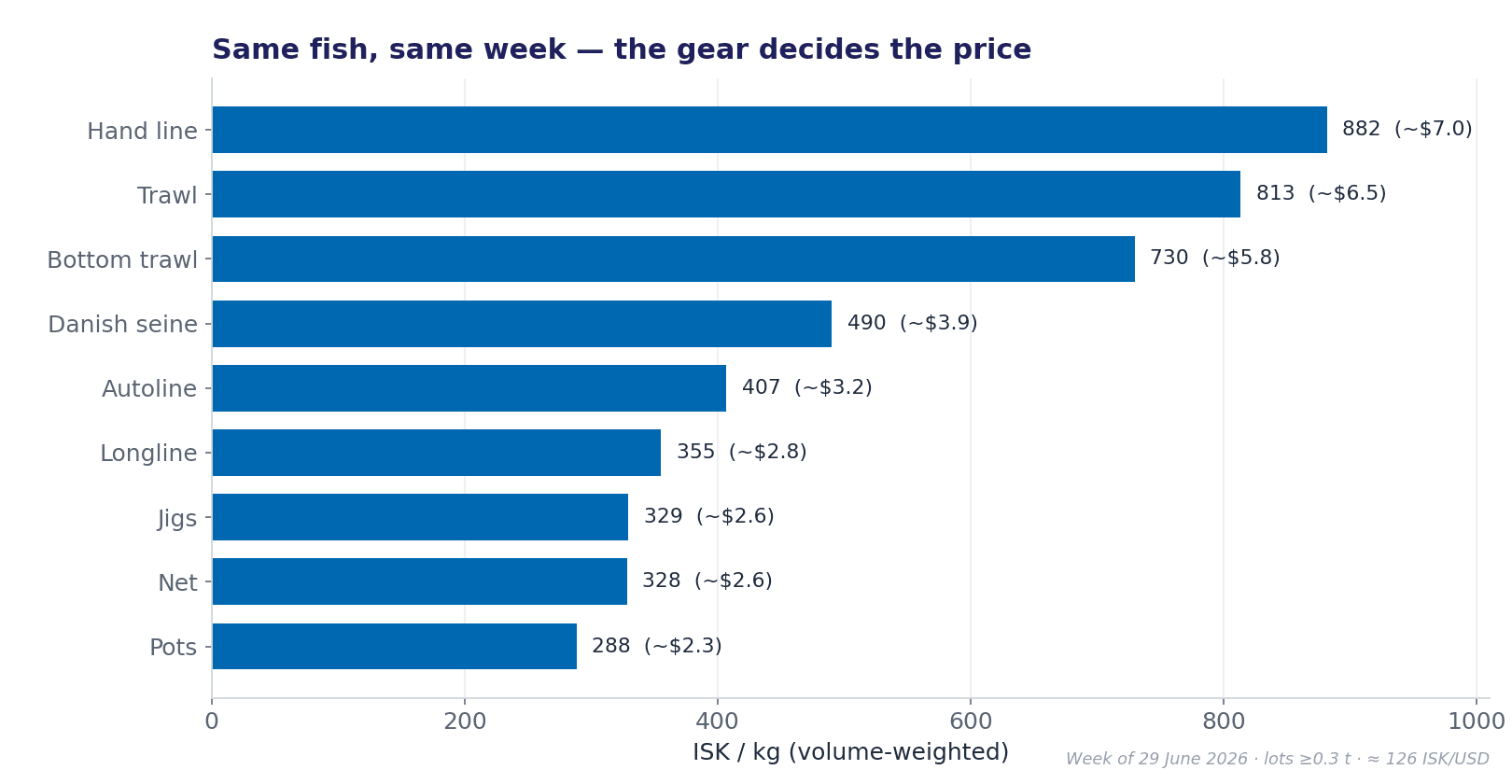

Here's why one "haddock price" is almost always misleading. In a single week, on the same auctions, the same species ran from ~330 ISK/kg (~$2.6) for net-caught fish to 860+ (~$7.0) for hand-line — a 2.7× spread. Reach back to the top lots of early June and you get all the way to 1,020 (~$8.1). Gear, size and condition move the price more than the calendar does, and whichever number you pick up off the floor, someone can quote a real receipt to back it.

One species, one week, ~2.7× spread by gear (lots ≥0.3 t). Which brick did you pick up? Source: Oceans of Data — RSF auction data.

The number wasn't wrong. The label was missing. That's not one loose interview — it's how most seafood "market intelligence" travels.

Why you should care

Because 1,020 doesn't stay on the radio. It walks into a contract call. A seller quotes it — "it's all over the market" — and a buyer with nothing to check it against either overpays or looks uninformed pushing back. For a whitefish trader moving 100 tonnes a week, being on the wrong side of $0.50/kg is about $50,000 in a single week. In this business the gap between a good week and a bad one is bigger than the whole margin, and it often turns on whose number wins the room.

Every producer and trader makes the same handful of calls: what to bid, when to sell, which market to push into, how hard to hold a price. Those are only as good as the number behind them — and the number that matters isn't "1,020," it's 1,020 (~$8.1) for top-grade fish, versus 730 (~$5.8) for the fillet grade, versus 520 (~$4.1) across the whole market, week of 29 June. Same fish, three decisions, three different answers. Know which one you're holding.

Anna Björk Theodórsdóttir

Founder and Managing Director Oceans